As a sun worshipper living somewhere especially prone to miserable weather, I’m always happier when the sun is shining and loathe to complain when the temperature rises. Nevertheless it’s been uncomfortably hot these past few weeks and my house plants are starting to wilt, my laptop is making worrying noises and the cat looks like he needs switching off and on again.

Something else that’s been burning bright has been the economic recovery this year, which has so far exceeded all expectations. As we move into the second half of the year, it seems an appropriate point to review what has happened in both the UK economy and the housing market so far in 2021, whilst considering what the rest of the year may have in store.

UK Economic Update

Being financial planners places us at an interesting intersection when it comes to the flow of economic data. Not only do we receive a constant flow of information from large financial institutions and business partners such as our investment partners Tatton, but also at an individual level, via our discussions with the many clients that we advise who are in business.

Automotive, construction, law, accountancy, scientific research, recruitment, design, sport, manufacturing, medicine, IT… Whilst their businesses may be diverse, a common feature they all share, is that they seem to be prospering in 2021. Long may it continue!

This certainly seems to be the overall trend across the UK, as the latest economic update from PwC accountants also shows.

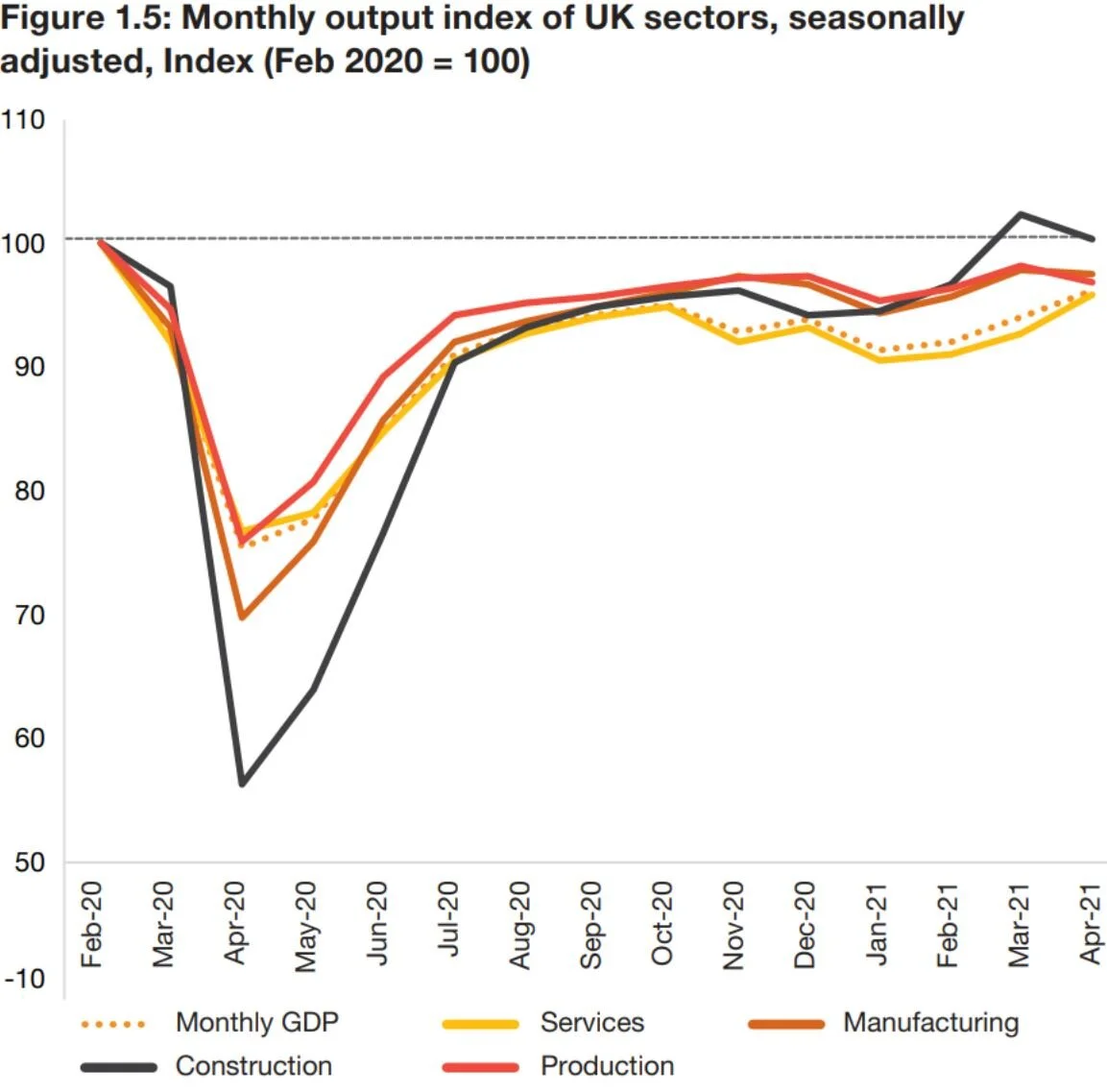

With the third national lockdown having reached it’s conclusion, it appears that the UK economy actually outperformed expectations despite the restrictions. Whilst there is a lag on the data being released, figures show that overall it grew by 2.3% in April for the third consecutive month – the fastest monthly growth rate since July 2020. This means that overall, around 83% of the output lost during the first national lockdown has now been recovered.

British businesses and the British public proved themselves remarkably resilient and adaptable during the pandemic and beyond, adjusting to the new world order surprisingly quickly. Meanwhile, whilst the UK government haven’t always showered themselves in glory during the pandemic, their fiscal support measures have been undeniably effective at protecting jobs and the economy, whilst the huge success of the UK vaccination program has also been a significant factor.

Looking forwards, PwC are expecting the recovery to continue it’s upward trend and as a result, they have upgraded their projections for 2021 and beyond. Since the Covid crisis hit, they have been running a pair of models, a ‘quick recovery’ and a ‘slow recovery’ model. In the face of unprecedented uncertainty, the two models were built to try to assess how quickly the UK economy might recover to it’s pre-Covid levels of activity and prosperity.

Both models have now been updated, with the ‘slow recovery’ model predicting a return to pre-crisis levels of economic prosperity by the end of 2022. The ‘quick recovery’ model meanwhile suggests this may be reached as early as the end of Q1 2022. That is an incredible 12 and 18 months sooner than previously thought and whilst nothing is guaranteed, it is a huge improvement whichever way you look at it. You can see their projections below:

Source: PwC Economic Outlook Jul 2021

There are a number of key factors that continue to drive the economic recovery going forwards. Firstly, we have household spending levels. The OBR (‘Office for Budget Responsibility’) estimates that household savings are now in the region of a staggering £180bn. If a good chunk of these savings get released into the economy via spending over the next few years, it could be a significant factor in the future growth of the UK economy.

At a government level meanwhile, Rishi Sunak has issued £15bn of Sovereign Green Bonds via NS&I, the proceeds of which will be used to finance infrastructure projects decarbonising the UK. Spending is expected to focus on zero-emissions buses, energy efficient housing schemes, offshore wind and climate adaptation measures, all of which has the potential to boost jobs and economic growth.

Then there is the potential for greater business investment, something that has been held back by many over the past 18 months. Many businesses have been choosing to roost on spare cash for safety, rather than risk investing it amidst pandemic uncertainty. If this situation begins to reverse as the economy continues to recover, it too could fuel a boom in economic activity.

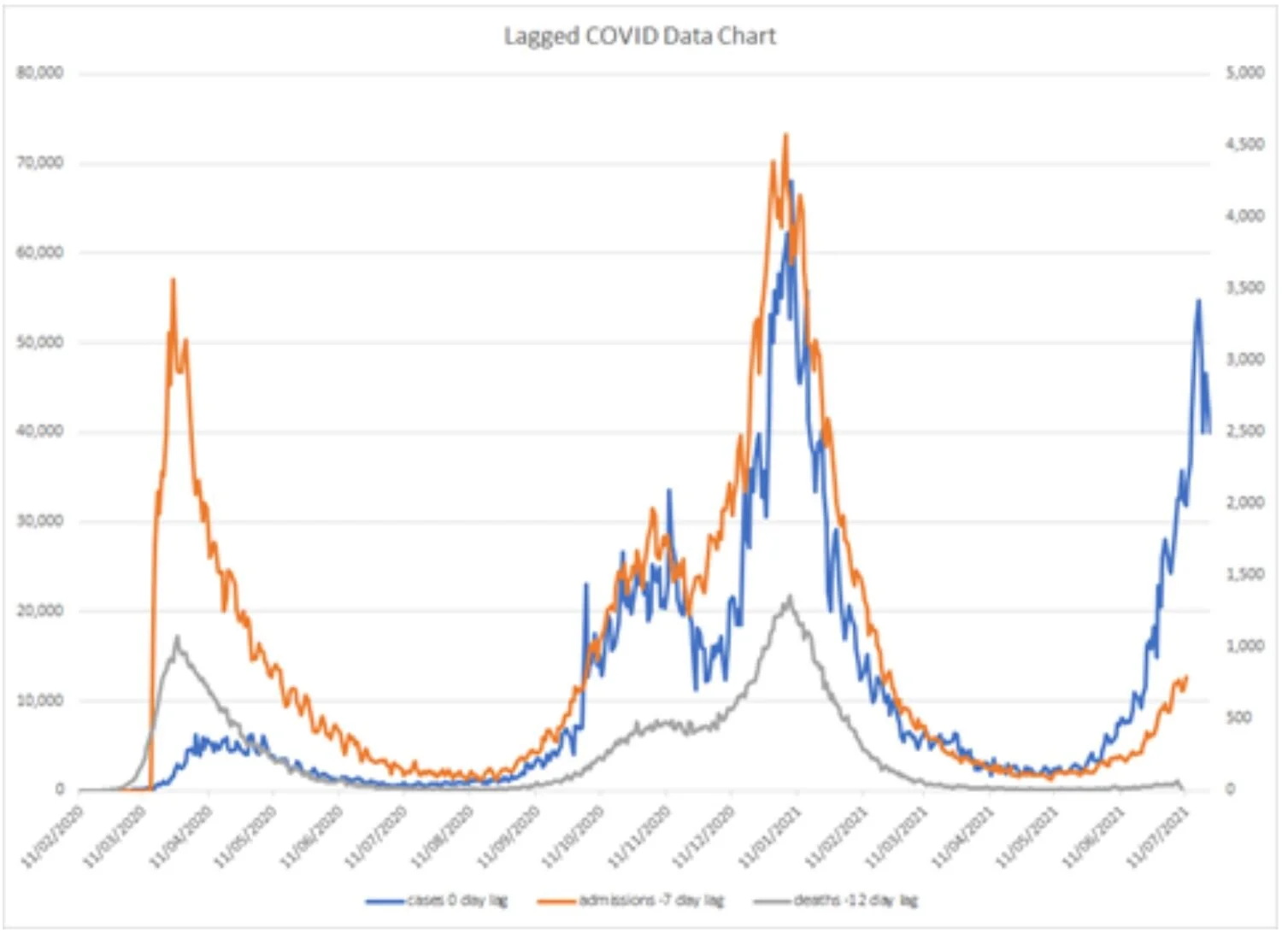

Risks remain however, with new Covid strains like the Delta variant having the potential to slow the recovery if they were to prompt a return to restrictions to protect public health. Daily cases have soared recently, though the key differences this time are that both hospitalisations and the death rate are far lower than they have been previously. The messaging from the government has changed in recent months however and the tone of the discussion is now about learning to live with the virus as opposed to just hiding ourselves away. Whilst there is a lag on the data, the figures do suggest that we are perhaps now moving past the peak, which is something that both the economy and investment markets will be pleased about.

Source: https://coronavirus.data.gov.uk/details/cases, TattonIM

One side effect of this rise in cases has been dubbed the ‘pingdemic’. Widespread adoption by the public of the NHS track and trace app has resulted in thousands of workers being told to self-isolate due to having come into close proximity with people who have tested positive. This is currently causing mass disruption to businesses and especially supply chains, leading to shortages of key goods and services and alarmingly bare supermarket shelves.

Then of course there are the trade challenges brought about by Brexit (remember that?!), as we continue to redefine trading relationships with our European cousins, whilst if inflation were to persist, it might force the Bank of England to increase interest rates and cut back stimulus, potentially slowing economic activity as a result.

The next major test for the economy is likely to be the end of the furlough scheme in the UK. Whilst previous concerns of a ‘big bang’ of unemployment now look unfounded, it also seems equally unlikely that all those that have been furloughed will simply slot back into their previous roles. Only time will tell, but things are certainly looking much brighter overall than they did twelve months ago.

UK Housing Market Update

When the pandemic first hit, many economic commentators and industry professionals (myself included) predicted a sharp - if temporary - decline in residential property prices, as a recessionary environment loomed large, with unprecedented restrictions to trade and social freedoms inbound.

However, take Rishi Sunak’s rabbit-in-a-hat stamp duty holiday, mix in an unexpected glut of household savings, then add plenty of pent-up demand and voila! A recipe for egg-on-face and a boom in the property market the likes of which have not been seen since the peak of the market back in summer 2007. Given the context of the situation I’m happy to have been proven wrong…

Halifax building society estimate house prices have risen by 9.5% in the 12 months leading up to June 2021, with Nationwide suggesting an even higher rate of growth of 13.4%.

his certainly tallies with our discussions with our clients. At almost every financial review we’ve been revising people’s home valuations upwards and reports are that buying activity is exceptionally strong across the country.

Reports show that all UK regions have experienced strong house price inflation since summer last year. Growth has been most pronounced in the Northwest, Yorkshire and The Humber, but whilst London saw the lowest growth in relative terms, it still remains the most expensive region by far, where the average home is now worth £500,000.

In addition to the stamp duty holiday, higher savings and pent-up demand, the rapacious appetite of Brits for home improvements must surely have also played a part. It seems like half the nation have been busy adding value to their homes, be it major redecorating projects, new bathrooms, kitchens, or extensions. It’s certainly been a boom time for the trades and a good time to be in the construction sector; assuming you can get hold of materials.

Given the better-than-expected performance of the UK economy and the likely continuation of many factors that have fuelled the boom, the outlook for the housing market remains positive for now. Ever rising household savings, coupled with the Chancellor’s extension of the job support scheme and deferred tax increases may all prove supportive. The new mortgage guarantee scheme meanwhile is likely to help more people than ever get onto the property ladder, whilst reducing borrowing costs. Welcome news no doubt to first time buyers who’ve seen the market run away from them over the last 12 months.

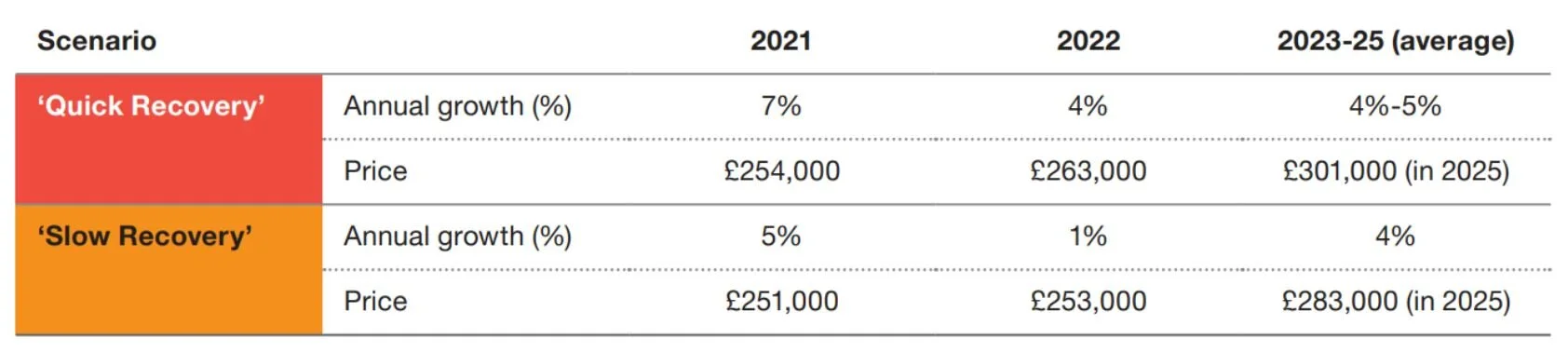

The table below summarises PwC’s expectations for the next four years, both in percentage terms and national average house prices:

Source: PwC UK Economic Outlook Jul 21

Despite the optimism, there are still some potential crunch factors however. The cessation of the job support scheme in September will likely have an impact on employment figures, which could in turn influence house prices. The aforementioned surge in the Delta variant meanwhile, could result in more lockdown measures, which might physically impede people’s ability to move, though admittedly this currently looks unlikely. If inflation were to get out of control meanwhile, the BoE may be compelled to raise interest rates, in turn impacting the mortgage market by increasing borrowing costs.

Closing Comments

So what does this mean to us?

Well, as investors, it looks like there is plenty of room for optimism. If the current economic prosperity continues, then there is potential for further stock market gains as a result. With other economies in the developed world also seeing strong recoveries (albeit some stronger than others), globally diversified portfolios like ours are well-positioned to benefit.

The potential for increased business investment is also an interesting topic, as when businesses successfully invest in their own growth and development, this can translate into higher future profits. This, combined with a greater willingness to unlock some of their cash reserves, may lead to higher dividends being paid on some of the shares we hold. With portfolios set up to reinvest dividends by default, this could also support higher long term returns.

Currently the biggest areas for concern are inflation and more virus variants. On the former point, experts still mostly agree that inflationary pressures should begin to subside towards the end of 2021, or early in 2022. If inflation did get out of hand however, this might force the hand of the Bank of England and other global central banks to increase rates, which could in turn spook equity markets, which are always skittish when it comes to monetary policy.

Perhaps more of an unknown is the future of the Covid virus itself. With the Delta variant already causing problems, most recently in the UK in the form of the ‘pingdemic’ (their term, not mine!), Covid itself shows no signs of abating just yet. We may be mostly vaccinated by now, but that still doesn’t mean there is no risk to public health from new strains, or to the labour market if current requirements for self-isolation don’t change any time soon.

Even if such things do temporarily derail the economic recovery, as long term investors, we know that a well-diversified portfolio and a bit of patience inevitably brings rewards. Our investors have benefitted from excellent performance throughout the pandemic and the subsequent recovery, and we have every faith in our investment partners Tatton to continue to deliver regardless of the ups and downs of the economic landscape.

From a home-owner’s perspective meanwhile, rising markets are largely irrelevant in the grand scheme of things, unless you’re planning a major move up, or down, the ladder. Even then, the effect of rising prices is often fairly neutral overall. For those looking to purchase a holiday home, or wanting to help children get on the ladder, they may find themselves needing to rustle up a little more cash than previously expected. For the property investors amongst our ranks meanwhile, you’ll no doubt be feeling rather pleased as things stand presently.

So with that I’ll sign off for now. I hope you’ve found this update useful and if you have any questions about it’s contents, or your broader finances, please don’t hesitate to get in touch.

Whatever the twists and turns of the economic recovery and what lies beyond, we’re here to ensure you receive the right advice to remain financially secure and on track to reach your goals.

Kind regards,